Written by the Chief of Department of Common Analysis of the Eastern Partnership

Eastern Digital Corridor

The global energy and logistics landscape was fundamentally altered on February 28, 2026, when the military escalation between the United States, Israel, and Iran led to the effective closure of the Strait of Hormuz.1 For the Eastern Digital Corridor and the broader Eastern Partnership (EaP) region—comprising Armenia, Azerbaijan, Georgia, Moldova, and Ukraine—this disruption represents far more than a transient spike in energy prices. It is a systemic shock that threatens the physical and economic foundations of digital transformation, reroutes the transit architecture of Eurasia, and creates lasting “scarring effects” that will persist long after a ceasefire is brokered.3 The Strait of Hormuz is the world’s most critical maritime chokepoint, facilitating the transit of approximately 20 to 21 million barrels of oil per day, representing 25% to 32% of the global seaborne crude trade.6Its closure has removed 20% of the world’s liquefied natural gas (LNG) supply from the market, primarily originating from Qatar and the United Arab Emirates, with no viable alternative export routes.8

The Energy Transmission Mechanism to the Eastern Partnership

The closure of the Strait of Hormuz acted as a transmission belt between regional war and the global economy, with the EaP region being particularly vulnerable due to its ongoing energy transition and the security challenges posed by the Russia-Ukraine war.5 On February 28, 2026, the day of the initial strikes on Tehran, vessel transits through the strait dropped to 105 ships, a significant decline from the average of 153 transits per day in preceding weeks.1 By March 2, total traffic fell to a mere 13 transits, representing only 8% of normal volume.1 This “soft closure” functioned as commercial deterrence, as the risk of military action, mines, and GNSS interference rendered the waterway commercially unusable.5

Oil Price Volatility and Fiscal Stability

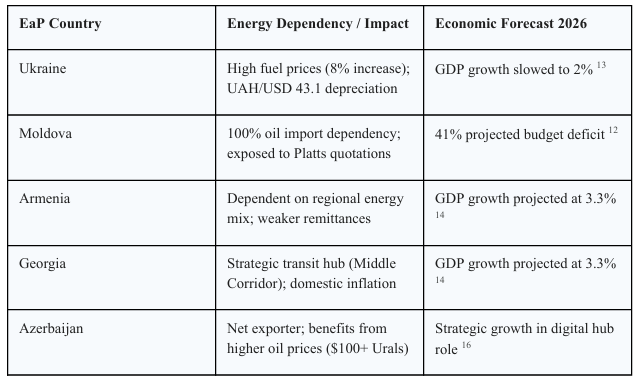

The immediate impact was a surge in Brent crude oil prices, which surpassed $100 per barrel on March 8, 2026, and peaked at $126 per barrel.2 For net energy importers like Moldova and Armenia, this volatility creates an “economic clock of war”.11In Moldova, the Energy Regulatory Agency (ANRE) noted that the

country is 100% dependent on imports of oil products, making it fully exposed to these external fluctuations.12 While daily price caps protect consumers from sudden spikes, the 14-day average of Platts

quotations means that high international prices are gradually but inevitably reflected in domestic petrol and diesel costs.12In Ukraine, fuel prices had already risen by 8% by February 2026, driven by higher energy costs and the depreciation of the hryvnia to 43.1 UAH/USD.13

The LNG Crisis and European Storage Reserves

The disruption of LNG transits through Hormuz removed over 300 million cubic meters per day of gas supply, totaling a loss of over 2 billion cubic meters (bcm) per week.8 Europe’s immediate vulnerability lies in refilling its gas storage, which stood below 30%—a five-year low—at the time of the escalation.10 Under EU regulations, storage must reach 90% capacity by December, requiring the injection of nearly 60 billion cubic meters during the 2026 refill season.10 Qatar, a major supplier to Europe, saw its Ras Laffan facilities go offline following military strikes.9 For Moldova and Ukraine, this means competing with wealthy Asian buyers (Japan, South Korea, Taiwan) for scarce LNG cargoes, driving prices to levels that threaten industrial viability and humanitarian stability in winter.10

Impact on the Digital Economy and ICT Supply Chains

The Strait of Hormuz is not only an energy corridor but a critical artery for the global Information and Communication Technology (ICT) sector.18 The digital transformation of the EaP region, a core goal of the Eastern Digital Corridor NGO, is directly impeded by the “cascading” disruptions in semiconductor manufacturing and raw material availability.3

Semiconductor Fabrication and Baseload Power

Advanced semiconductor fabrication facilities in Taiwan and South Korea, which account for 68% of global production, require vast, continuous electricity supplies to operate lithography systems.20 These facilities rely heavily on imported LNG to maintain the stability of their power networks.20 Even a momentary drop in voltage or a brief interruption lasting fractions of a second can destroy tens of thousands of silicon wafers, causing losses worth hundreds of millions of dollars.20 The sudden evaporation of Gulf LNG supply has placed these foundries under severe strain, leading to a “growth disruption” in the supply of components needed for AI servers, 5G base stations, and consumer electronics across the EaP region.20

Critical Raw Materials: Helium, Sulfur, and Bromine

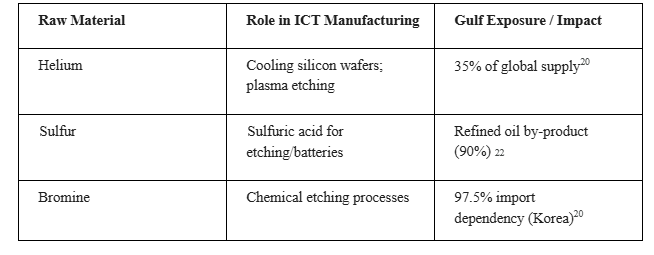

The semiconductor industry is highly sensitive to the supply of specialized chemicals and gases that transit or are produced in the Gulf region.19

● Helium: The Gulf region represents roughly 35% of the global helium supply, a critical by-product of LNG liquefaction used for cooling silicon wafers.20 The semiconductor sector accounts for 24% to 30% of total global helium demand.20

● Sulfur: More than 90% of the world’s sulfur supply is a by-product of oil refining.22 Sulfur is essential for producing sulfuric acid, a key chemical for semiconductor etching and battery components.22

● Bromine: South Korean factories import 97.5% of their bromine from the Dead Sea coast for chemical etching processes.20

The disruption of these inputs means that even after a ceasefire, the backlog in semiconductor production will persist for months or years, as the replenishment of global helium and sulfur stocks depends on the restoration of Gulf oil and gas production.22

Naphtha Key petrochemical input for plastics 37% of East Asian supply7

Impact on Subsea Digital Infrastructure and 5G Rollout

The conflict has transformed the Strait of Hormuz from a promising digital corridor into an active war zone, shattering the assumption that the Middle East is a secure digital transit point.25 This has direct implications for the Eastern Digital Corridor’s connectivity with global data hubs.

Stalled Subsea Cable Projects

Several major subsea cable systems have seen their progress halted or their existing infrastructure threatened:

● 2Africa Pearls: This extension of the 45,000-km 2Africa system, meant to serve over 3 billion people, was suspended mid-installation.25 Alcatel Submarine Networks (ASN) was forced to issue force majeure notices as repair and cable-laying vessels, such as the Ile De Batz, could no longer safely operate in the Persian Gulf.25

● SEA-ME-WE 6 (SMW6): This major corridor connecting Asia and Europe had already shifted toward a terrestrial bypass through Saudi Arabia to avoid the Red Sea.25 However, the Gulf Extension (Al Khaleej Cable System) is now indefinitely delayed, straining capacity on the critical Singapore-to-Europe route.25

● Fibre in Gulf (FIG): This project, designed to bypass the Red Sea via a land route through Iraq and Turkey, now faces an uncertain future as the Persian Gulf itself has become a battlefield.25

Maintenance and Repair Vulnerabilities

The “double chokepoint” of the Red Sea and the Strait of Hormuz means that any new damage to existing cables could result in outages lasting months rather than hours.21 Repair vessels cannot enter territorial waters without security clearance, and ongoing hostilities prevent the safe deployment of technicians.26 This vulnerability is mirrored in the Black Sea, where the Russia-Ukraine war has already elevated risks for merchant ships and subsea infrastructure.28 Persistent GNSS jamming, sea mines, and drone strikes in the Black Sea make the maintenance of cable landing stations in Georgia and Ukraine increasingly precarious.28

The Rise of the Middle Corridor as a Strategic Alternative

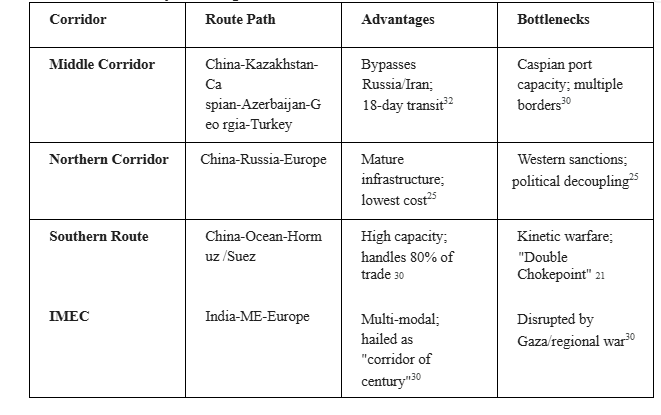

A significant outcome of the Hormuz crisis is the rapid strategic re-orientation toward the Middle Corridor (Trans-Caspian International Transport Route or TITR).30 This route connects China to Europe via Kazakhstan, the Caspian Sea, Azerbaijan, Georgia, and Turkey, bypassing both Russia and Iran.31

Growth and Capacity Dynamics

Since 2022, logistics actors have increasingly turned to the Middle Corridor as a resilient alternative to

maritime routes.34 Freight volumes grew from 840,000 tons in 2021 to 4.5 million tons in 2024.30 The 2026 Hormuz crisis is expected to triple these volumes by 2030, with a forecast of 11 million tonnes of freight.32 For EaP countries, particularly Azerbaijan and Georgia, this presents a historic opportunity to establish themselves as central transit hubs.32

Digitalization and “Soft Infrastructure”

The success of the Middle Corridor depends as much on digital infrastructure as on physical rails and ports.16 Azerbaijan is investing in transforming itself into a transnational digital hub through the “Digital Silk Way” project.16

● Customs Automation: Azerbaijan’s State Customs Committee partnered with Huawei to modernize its customs system through a “single window” system and a unified center for transit freight management.16

● Fiber Optic Backbone: The Trans-Caspian Fiber Optic Cable Project, currently in development, will connect Azerbaijan and Kazakhstan via the bottom of the Caspian Sea, creating a digital telecommunications corridor between Europe and Asia.16

● Facilitation Tools: The use of TIR and eTIR (digital customs transit) is slashing transit times by 80% and costs by 50% along the route.34

Geopolitical Realignment and Influence Shifts

The closure of the Strait of Hormuz has created new geopolitical leverage for adversaries of the Western-led maritime order, primarily Russia and China, while weakening the economies of the Eastern

Partnership.17

Russia’s Gains from Global Volatility

Despite being sanctioned, Russia has emerged as a strategic beneficiary of the Hormuz crisis:

● Fiscal Capacity: With oil prices rising, Russia is estimated to make billions of extra dollars each month, which finances its offensive in Donbas.17 The price of Urals crude in Russian ports has exceeded $60 per barrel, while delivered prices to India reached $100.17

● Fertilizer Diplomacy: Russia is the world’s largest exporter of fertilizer, and Belarus is a major player in potash.38 As Gulf-based fertilizer plants (accounting for 30% of nitrogen fertilizer) shut down due to energy shortages, Russia and Belarus are well-positioned to fill the gap, gaining leverage over global food supply chains.9

● Military Resource Diversion: The conflict in the Middle East has diverted key Western military supplies, such as Patriot air defense interceptors, away from Ukraine, leaving its energy and digital infrastructure more vulnerable.39

China’s “Favored Nation” Status in the Gulf

China has mitigated its exposure to the Hormuz closure through long-term planning and diversified overland energy pipelines.40 China imports 55% of its oil from the Middle East, but its strategic oil reserves (enough for 18 days of national consumption) and pipelines through Russia and Myanmar provide a buffer.40 Critically, reports suggest that Iran has allowed only Chinese-affiliated vessels to

transit the Strait of Hormuz, enabling Beijing to maintain its industrial supply chains while competitors face rerouting costs.41 This crisis could see the petrochemical and semiconductor sectors further concentrate in China, giving Beijing additional leverage over the global digital economy.38

The “After the Ceasefire” Reality: Scarring Effects and Long-term Burden

A ceasefire in the Persian Gulf will not provide an immediate panacea for the Eastern Partnership. The “scarring effects” of the conflict ensure that a return to normal operations will be slow and expensive.4

Five-Year Repair Horizons for Energy Infrastructure

The physical damage to energy infrastructure in the Gulf is extensive. Qatari authorities have declared that it will take up to five years to repair the damage done to its gas facilities during the war.39 This long-term curtailment of LNG supply means that energy prices in Europe and the EaP region will remain structurally higher than pre-2026 levels for years.4 For the Eastern Digital Corridor, this translates into permanently higher operating costs for data centers and digital hubs.4

Permanent Shifts in Insurance and Risk Assessment

Shipping insurance premiums have been repriced across multiple lines, including war risk, energy,

political violence, and trade credit.5 Even after a ceasefire, insurers are expected to maintain high premiums for the Gulf and Red Sea, treating them as permanently high-risk zones.5 This “risk premium” is a long-term burden on global trade, forcing a permanent shift toward terrestrial alternatives like the Middle Corridor and Arctic routes like Polar Connect.21

Financial Instability and Stagflation Risks

The 2026 energy shock has reignited fears of stagflation—rising prices coupled with slowing growth.38 For import-dependent EaP countries, this means weaker trade balances and greater currency pressure.5 The Federal Reserve’s hard-won credibility on inflation was challenged as top-line and core PCE moved into the 3.5% to 4% range in early 2026.44 This global tightening of financial conditions makes it harder for EaP nations to access the capital needed for large-scale digital infrastructure projects.5

Structural Sourcing Shifts: “Friendshoring” and Resilience

The crisis marks an “inflection point” for global supply chains, moving away from cost-optimization toward geographic diversification and energy security.23 Companies are reassessing structural dependencies, opting for “nearshoring” and “friendshoring”.41 For the Eastern Digital Corridor, this represents a shift toward:

1. Geographically Diversified Refining: Reducing reliance on Gulf-based refined products (naphtha, diesel).23

2. Inventory Buffering: Moving from “just-in-time” to “just-in-case” inventory management for critical digital components.3

3. Regional Maritime Security: Investing in layered risk mitigation strategies, including private maritime security and real-time vessel tracking, even for Black Sea transits.41

Strategic Implications for the Eastern Digital Corridor NGO

The closure of the Strait of Hormuz has fundamentally changed the mission and operational environment of the Eastern Digital Corridor. The path forward requires a focus on resilience, regional integration, and energy-independent digital infrastructure.

Building Energy-Resilient Digital Hubs

Since digital infrastructure is one of the most energy-intensive industrial processes, the EaP region must decouple its data centers from global energy shocks.22 This includes:

● Integrating Renewables: Accelerating the deployment of large-scale nuclear and renewable energy projects to provide stable, low-cost baseload power for foundries and data hubs.23 ● Developing Local Chemical Supplies: Investigating regional sources for sulfur and high-purity gases to mitigate the “helium and sulfuric acid” bottleneck.20

Optimizing the Middle Corridor for Digital Trade

The Middle Corridor is the EaP’s best defense against maritime chokepoints, but it requires further “digitalization of the entire transport route”.16

● Synchronized Customs: Implementing the “single window” and eTIR across all EaP states to transform the corridor into a predictable and competitive resilient trade artery.16

● Interoperability: Addressing the maritime links in the Caspian and Black Seas, where port equipment often cannot handle containerized electronics or ICT hardware.36

Securing Subsea and Terrestrial Redundancy

The Eastern Digital Corridor must advocate for a network of multiple reliable corridors.30 This means:

● Black Sea Connectivity: Prioritizing the maintenance and security of Black Sea subsea cables, despite the kinetic risks, to maintain direct links to European data hubs.28

● Arctic and Northern Alternatives: Monitoring the development of the “Polar Connect” and “TEA NEXT” projects as long-term redundancies that bypass the Middle Eastern “Double Chokepoint”.25

Conclusion: The Long Road to Reconstruction

The 2026 Strait of Hormuz crisis has proven that the future of technology is not just written in code but determined by the security of narrow shipping lanes and the stability of global energy markets.22 For the Eastern Partnership, the conflict has been an expensive lesson in the dangers of structural dependency. Even as a ceasefire approaches, the economic and logistical landscape of the EaP will be defined by the “scarring” of Gulf energy infrastructure, the repricing of maritime risk, and the strategic rise of the Middle Corridor as the new digital and physical spine of Eurasia. The Eastern Digital Corridor must lead the effort to build a regional digital ecosystem that is not only faster and more connected but also robust enough to absorb the next systemic shock to the global order.

Works cited

1. No One, Not Even Beijing, Is Getting Through the Strait of Hormuz, accessed April 9, 2026, https://www.csis.org/analysis/no-one-not-even-beijing-getting-through-strait-hormuz 2. 2026 Strait of Hormuz crisis – Wikipedia, accessed April 9, 2026,

2. https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis

3. Strait of Hormuz Closure Disrupting Global Supply Chains, accessed April 9, 2026, https://www.eawlogistics.com/strait-of-hormuz-closure-disrupting-global-supply-chains/

4. Strait of Hormuz: Global supply chain at risk | Roland Berger, accessed April 9, 2026, https://www.rolandberger.com/en/Insights/Publications/Managing-the-short-and-long-term -effects-of-Strait-of-Hormuz-tensions.html

5. Global Markets and the Strait of Hormuz: The Economic Shockwaves of the Iran War, accessed April 9, 2026,

https://www.stimson.org/2026/global-markets-and-the-strait-of-hormuz-the-economic-sho ckwaves-of-the-iran-war/

6. Chart: Quarter of Maritime Oil Trade Flows Through Strait of Hormuz | Statista, accessed April 9, 2026,

https://www.statista.com/chart/35914/destination-maritime-crude-oil-strait-of-hormuz/

7. Oil Products Arbs and Flows: All Eyes On Strait of Hormuz – BloombergNEF, accessed April 9, 2026,

https://about.bnef.com/insights/commodities/oil-products-arbs-and-flows-all-eyes-on-strait -of-hormuz/

8. The Middle East and Global Energy Markets – Topics – IEA, accessed April 9, 2026, https://www.iea.org/topics/the-middle-east-and-global-energy-markets

9. Hormuz Shutdown: Impact on Dry Bulk, LNG & Trade Risk … – Kpler, accessed April 9, 2026,

https://www.kpler.com/blog/how-the-strait-of-hormuz-shutdown-is-disrupting-dry-bulk-ln g-freight-and-trade-compliance

10. How the Iran war could trigger a European energy crisis – Atlantic Council, accessed April 9, 2026,

https://www.atlanticcouncil.org/dispatches/how-the-iran-war-could-trigger-a-european-ene rgy-crisis/

11. Disruption in the Strait of Hormuz is a global inflation, shipping and growth story – LSE Business Review, accessed April 9, 2026,

https://blogs.lse.ac.uk/businessreview/2026/03/12/disruption-in-the-strait-of-hormuz-is-a-g lobal-inflation-shipping-and-growth-story/

12. Moldovan Energy Regulatory Agency says events in Persian Gulf region influence international oil prices – Moldpres.md, accessed April 9, 2026,

https://www.moldpres.md/eng/economy/moldovan-energy-regulatory-agency-says-events in-persian-gulf-region-influence-international-oil-prices

13. Escalation in the Middle East and energy infrastructure attacks …, accessed April 9, 2026, https://kse.ua/about-the-school/news/escalation-in-the-middle-east-and-energy-infrastructu re-attacks-increase-pressure-on-prices-the-exchange-rate-and-the-economy-ukraine-month ly-economic-update/

14. Global Economic Prospects — January 2026 – The World Bank, accessed April 9, 2026, https://thedocs.worldbank.org/en/doc/7ce50b5aa95bef66048680bba9926ec8-0050012026/r elated/GEP-Jan-2026-Analysis-ECA.pdf

15. Transnistria Gas Crisis: Energy Security Emergency – Discovery Alert, accessed April 9, 2026,

https://discoveryalert.com.au/energy-security-2026-european-dependencies-vulnerabilities/

16. The Rising Significance of the Middle Corridor – Baku Dialogues …, accessed April 9, 2026,

https://bakudialogues.idd.az/articles/the-rising-significance-of-the-middle-corridor-18-10- 2022

17. Russia Analytical Report, March 30–April 6, 2026, accessed April 9, 2026, https://www.russiamatters.org/news/russia-analytical-report/russia-analytical-report-march -30-april-6-2026

18. Strait of Hormuz: from helium to aluminium, the non-oil raw materials crisis, accessed April 9, 2026,

https://www.renewablematter.eu/en/strait-of-hormuz-helium-aluminium-non-oil-raw-mater ials-crisis

19. Analysis: The Hormuz Crisis and Its Implications for the Semiconductor Industry,

accessed April 9, 2026,

https://www.techinsights.com/blog/analysis-hormuz-crisis-and-its-implications-semicondu ctor-industry

20. Strait of Hormuz Closure: Strategic Implications for the Global Semiconductor Industry, accessed April 9, 2026,

https://www.habtoorresearch.com/programmes/hormuz-closure-global-semiconductor/

21. Escalating Middle East conflicts have caused multiple supply shocks – CGTN, accessed April 9, 2026,

https://news.cgtn.com/news/2026-04-06/Escalating-Middle-East-conflicts-have-caused-mu ltiple-supply-shocks–1M7pJqLVGsE/index.html

22. Strait of Hormuz: Disrupting Global Tech – Morgan Stanley, accessed April 9, 2026, https://www.morganstanley.com/insights/podcasts/thoughts-on-the-market/strait-of-hormu z-disrupting-global-tech-shawn-kim

23. Strait of Hormuz crisis marks “inflection point” for global supply chains | Cornell Chronicle, accessed April 9, 2026,

https://news.cornell.edu/media-relations/tip-sheets/strait-hormuz-crisis-marks-inflection-p oint-global-supply-chains

24. Hormuz and the Export of Chaos into Global Supply Chains – ORF Middle East, accessed April 9, 2026,

https://orfme.org/expert-speak/hormuz-and-the-export-of-chaos-into-global-supply-chains/

25. War in the Gulf Severs the World’s Digital Arteries: How the Iran …, accessed April 9, 2026,

https://www.submarinenetworks.com/en/nv/insights/war-in-the-gulf-severs-the-world-s-di gital-arteries

26. From Barrels to Bandwidth: A New Chokepoint is Emerging in the Gulf, accessed April 9, 2026,

https://betterworldcampaign.org/peace-and-security/from-barrels-to-bandwidth-a-new-cho kepoint-emerges-in-the-red-sea

27. Iran’s Cable Threat: Disrupting Global Data Flow and Impacting Technology Shares – Bitget, accessed April 9, 2026, https://www.bitget.com/news/detail/12560605312939

28. Maritime security in the northern Black Sea: Operational realities and emerging risks – Skuld, accessed April 9, 2026,

https://www.skuld.com/topics/port/port-news/europe/maritime-security-in-the-northern-bla ck-sea-operational-realities-and-emerging-risks/

29. SUBSEa CABLES – What is at stake? – ENISA, accessed April 9, 2026, https://www.enisa.europa.eu/sites/default/files/publications/Undersea%20cables%20-%20 What%20is%20a%20stake%20report.pdf

30. The Middle Corridor in the Spotlight | German Marshall Fund of the …, accessed April 9, 2026, https://www.gmfus.org/news/middle-corridor-spotlight

31. Trans-Caspian International Transport Route – Wikipedia, accessed April 9, 2026, https://en.wikipedia.org/wiki/Trans-Caspian_International_Transport_Route

32. Why the Middle Corridor matters amid a geopolitical resorting – Atlantic Council, accessed April 9, 2026,

https://www.atlanticcouncil.org/content-series/ac-turkey-defense-journal/why-the-middle-c orridor-matters-amid-a-geopolitical-resorting/

33. The Growing Importance of the Middle Corridor as an Energy Transport Route, accessed April 9, 2026,

https://hagueresearch.org/the-growing-importance-of-the-middle-corridor-as-an-energy-tra nsport-route/

34. Minutes, not maps: making borders work for the Middle Corridor – IRU, accessed April 9, 2026,

https://www.iru.org/news-resources/newsroom/minutes-not-maps-making-borders-work-m iddle-corridor

35. Türkiye’s Connectivity and Multilateral Transportation Policy, accessed April 9, 2026, https://www.mfa.gov.tr/turkiye_s-multilateral-transportation-policy.en.mfa

36. Transport Connectivity in Central Asia: Strengthening Alternative Trade Corridors between Europe and Asia – International Transport Forum, accessed April 9, 2026, https://www.itf-oecd.org/sites/default/files/ukraine-trade-corridors.pdf

37. World Bank Document, accessed April 9, 2026,

https://openknowledge.worldbank.org/server/api/core/bitstreams/44313ea3-6d0a-5bb0-a05 8-8ac116b1beee/content

38. The Strait of Hormuz crisis will ripple across plastics and food supply chains, helping Beijing and Moscow, hurting Americans – Atlantic Council, accessed April 9, 2026, https://www.atlanticcouncil.org/blogs/energysource/the-strait-of-hormuz-crisis-will-ripple across-plastics-and-food-supply-chains-helping-beijing-and-moscow-hurting-americans/

39. Watch List 2026 – Spring Edition | International Crisis Group, accessed April 9, 2026, https://www.crisisgroup.org/euw/global/watch-list-2026-spring-edition

40. Why the Iran war won’t shake China’s Middle East strategy – ThinkChina.sg, accessed April 9, 2026,

https://www.thinkchina.sg/economy/why-iran-war-wont-shake-chinas-middle-east-strategy ?ref=top-hero

41. Strait of Hormuz Disruption and Implications for Risk, Continuity, and Strategic Response, accessed April 9, 2026,

https://thunderbird.asu.edu/thought-leadership/insights/strait-hormuz-disruption-and-impli cations-risk-continuity-and-strategic

42. Hormuz closure impacting many lines and set to trigger tougher mid-year renewals: Howden Re – Commercial Risk, accessed April 9, 2026,

https://www.commercialriskonline.com/hormuz-closure-impacting-many-lines-and-set-to-t rigger-tougher-mid-year-renewals-howden-re/

43. Narratives of Disruption: How Iranian Messaging Targets Global Energy Supply Chains, accessed April 9, 2026,

https://edgetheory.com/resources/narratives-of-disruption-how-iranian-messaging-targets-g lobal-energy-supply-chains

44. Why an energy shock is a nightmare for the Fed | RSM US, accessed April 9, 2026, https://rsmus.com/insights/economics/why-energy-shock-is-a-nightmare-for-the-fed.html

45. Strait of Hormuz: 6 Experts Have Say on Supply Chain Crisis, accessed April 9, 2026, https://supplychaindigital.com/news/strait-of-hormuz-crisis-qa-what-next-for-global-suppl y-chains